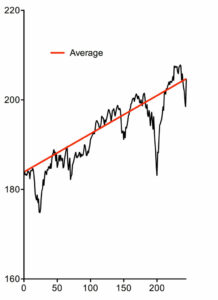

The above graph illustrates the hypothetical gains an investor could have made if they had invested at the lowest point. However, the likelihood of accurately timing the dip is slim. The fear of missing out (FOMO) often leads investors to make purchases at market highs, which can result in panic selling during market downturns and significant financial loss.

Do you know why inflation happens? Read here>>> How inflation affects retirement: A Mission Critical Article

Investing discipline can be challenging to maintain, especially when emotions run high in volatile markets. By adhering to a fixed investment plan through dollar-cost averaging and implementing a budget rule like the 50/30/20 principle, you can effectively balance your short-term expenses with your long-term savings goals. This approach can help you stay focused and confident in your investment strategy, even during market turbulence.

Consistency and discipline are essential to investment success, and dollar-cost averaging is just one of many tools to build up those necessary traits.

Don’t Miss Our Other Free Resources! >>> Mission Critical Educational Videos

Portfolio Rebalancing

As previously stated, a common problem among investors is snatching up investment vehicles at inflated prices and then dumping them once the bubble bursts. But what if I tell you that it’s possible to buy low and sell high consistently – a scenario that every investor aspires to achieve? You can simplify the process by adhering to the principles of diversification and appropriate asset allocation. However, this process is challenging from a psychological perspective due to the necessity of offloading higher-performing assets. Nevertheless, following these rules usually results in long-term gains. Here’s how it works.

You can read about inflation-fighting, wealth-building investment ideas here —> Protect Your Savings from Inflation in 2023!

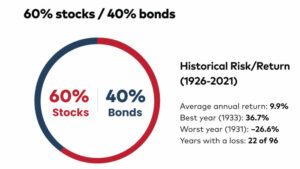

A fairly aggressive growth-oriented investment portfolio consists of stocks and bonds with a 60/40 allocation, a fantastic position for someone with a lengthy investment horizon.

A well-diversified portfolio should also contain a segmentation of stocks and bonds within different industry sectors. The S&P 500 serves as an excellent substitute and example of a diversified and comprehensive investment portfolio.

- Information technology – 28.7%

- Healthcare – 13.1%

- Consumer Discretionary – 12%

- Financials – 11.3%

- Communication Services – 10%

- Industrials – 7.8%

- Consumer Staples – 6.1%

- Energy – 3.4%

- Real Estate – 2.7%

- Materials – 2.5%

- Utilities – 2.5%

When a particular industry or sector of a portfolio starts to outperform the others, it may become over-represented in the portfolio, leading to an imbalance. On the other hand, when a sector underperforms, its proportion in the portfolio will shrink.

To maintain the desired asset allocation, the investor must sell the excess growth of the outperforming assets and reallocate the proceeds into the underperforming assets. This process of selling high and buying low enables investors to take advantage of market fluctuations and potentially increase their returns over the long term.

Dollar-cost averaging combined with portfolio rebalancing

Dollar-cost averaging as a method of portfolio rebalancing involves consistently contributing a fixed amount of money into your investment account, such as through payroll deductions. This money is then automatically invested into your assets according to your established asset allocation strategy.

By consistently and systematically adding money, you can help maintain your desired asset allocation by automatically purchasing more of what is needed in your portfolio to keep it in line with your established strategy. This method provides a more gradual and disciplined approach to portfolio rebalancing while reducing the need to make emotionally-charged decisions to sell winning assets.

Dividend stocks grow your portfolio in flat markets (as long as you reinvest them!)

Dividend-paying stocks provide an excellent opportunity to counteract the effects of market volatility. This is because the income they provide helps to anchor the stock price closer to its average value. After accounting for dividends, stock prices need to experience a more significant drop to result in a decline in value.

Moreover, the income from dividends helps to fight the impact of inflation, as companies often pass on increased operating costs to consumers, leading to higher earnings and dividend payouts. Finally, reinvesting dividends can result in a compounding effect, with larger and larger dividends leading to more significant overall growth.

Let’s look at one example of how dividend stocks can lead to portfolio growth in a flat market. The Dow Jones, consisting of 30 blue-chip, dividend-paying stocks, as opposed to growth stocks, which don’t typically pay dividends because they reinvest their earnings, had a mainly flat period in the 1960s and early 1970s. Between 1965 and 1972, the total average return was only 1.659%. However, by reinvesting the dividends, the overall returns shoot up to over 30%!

No matter the state of the economy, staying disciplined and following these investment strategies can help you weather a bear market or recession. Additionally, avoiding panic-driven decisions and risky investments makes you more likely to come out in a strong position.

If you’d like a review of your portfolio, don’t hesitate to click the button and schedule a meeting.